February 2023 - Ryman looks like a classic value trap

by Stephen Bennie 2023-02-07

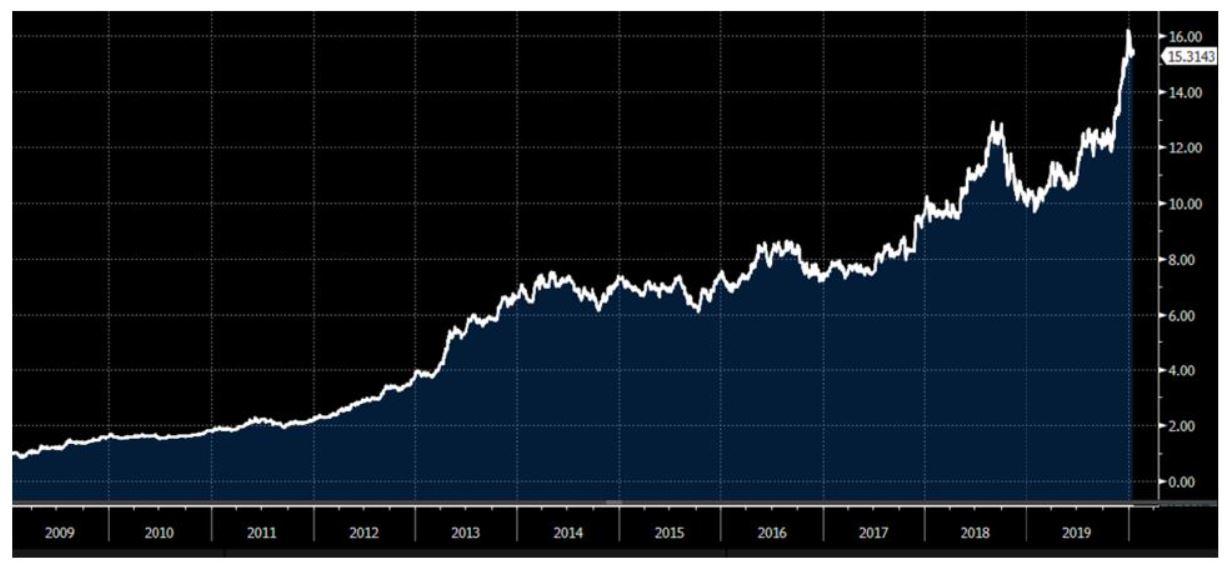

It is a fact that Ryman Healthcare (Ryman) enjoyed a stellar run from 2009 to 2020 up nearly 1,800% from 85c to $16. It can also be readily assumed that a bunch of investors made good money from holding Ryman over parts of this 10-year period. Sustained periods of strong returns that create investors wealth often become what are referred to as “market darlings”. These are companies that can seemingly do no wrong; their executives regularly win the Deloitte CEO of the year award, the company is rated a buy by all the brokers, investor days are like a trip to Mecca for the converted and its share price just keeps going up. Some companies, such as a Microsoft or a Coca-Cola Company, can sustain this positive cycle of love for decades but others have just completed the first stage of becoming a potential value trap, because the first requirement of a classic value trap is that it used to be a “market darling”. And Ryman was clearly an in favour NZX listed business as 2020 began.

Chart showing a stellar decade of returns for Ryman Healthcare

Source: Bloomberg

Another important ingredient for creating a value trap is a business that doesn’t generate significant positive operating cash flows. The retirement village business model has several key positives; leverage to rising residential property prices, low realised corporate tax rates and free capital from its customers. It should be noted though that exposure to property prices is less exciting when prices are going down as they have in the past year. And the low realised corporate tax rate while notionally a plus for shareholders does also highlights that the majority of profit before tax is non-taxable, meaning operating cash flows are significantly lower than reported profit.

The third positive is hard to see any issues with though, no shareholder ever said no to free capital and the retirement village is chock a block with free capital. When residents move in, they pay full freight for their unit, let’s call it $800k a pop, which Ryman holds until the residents check out. At that point there is a squaring up of the ledger with Ryman getting its deferred management fee and relatives of the ex-residents getting back the balance of what was the free capital. In the period that the residents lived in the unit, Ryman were able to use their $800k to build more units and grow operations despite its low operating cash flow, without needing to utilise bank debt. A neat trick and key part of why Ryman became such a darling of the market.

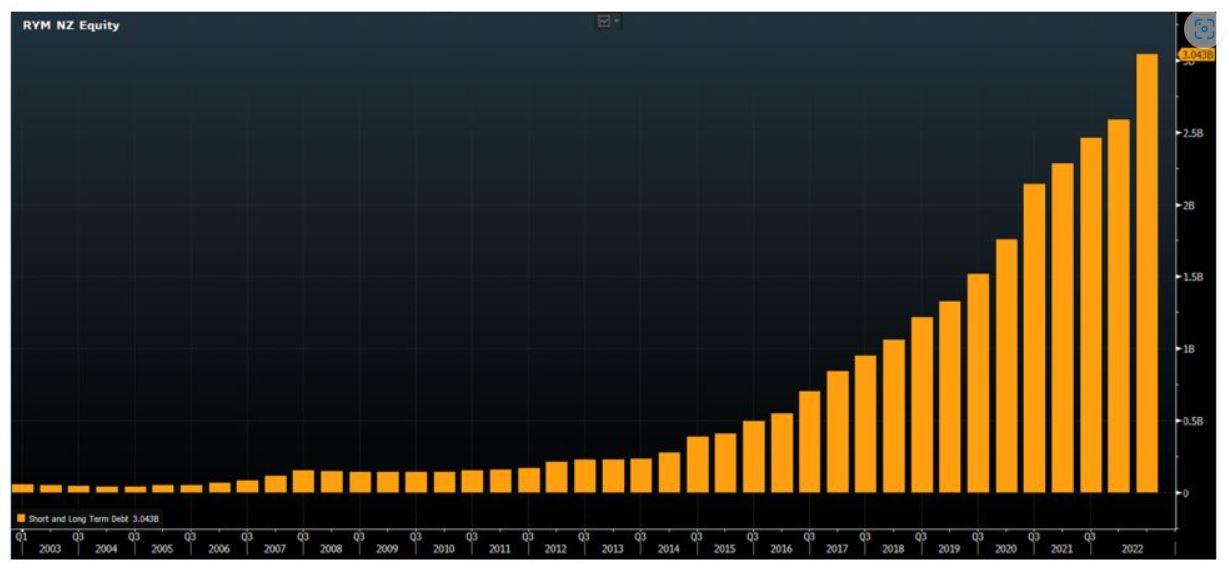

Chart showing Ryman’s stellar growth in debt

Source: Bloomberg

This makes it all the more surprising when you come to chart Ryman’s debt over the past two decades. It starts out as at low levels as you would expect given the free capital the business can access from its residents. At the beginning of its stellar decade, in 2009, total debt stood at $142m, which was more by way of liquidity management than a structural debt burden. However, as the chart shows that changed dramatically over ensuing years. Part of becoming a market darling is growth in earnings and to grow faster Ryman needed more capital and given its weak operating cash flow metrics the extra capital had to be borrowed from the banks. In recent months Ryman has signalled that it intends to address debt levels but the damage has arguably already been done. At its current share price, say $5.70, Ryman has a market capitalisation of $2.8 billion which is lower than its net debt of $3 billion. So here we have another part of a value trap, debt levels higher than the current market capitalisation. It’s not a definite outcome but it’s generally a situation that culminates in a rights issue or a share placement to meaningfully reduce net debt.

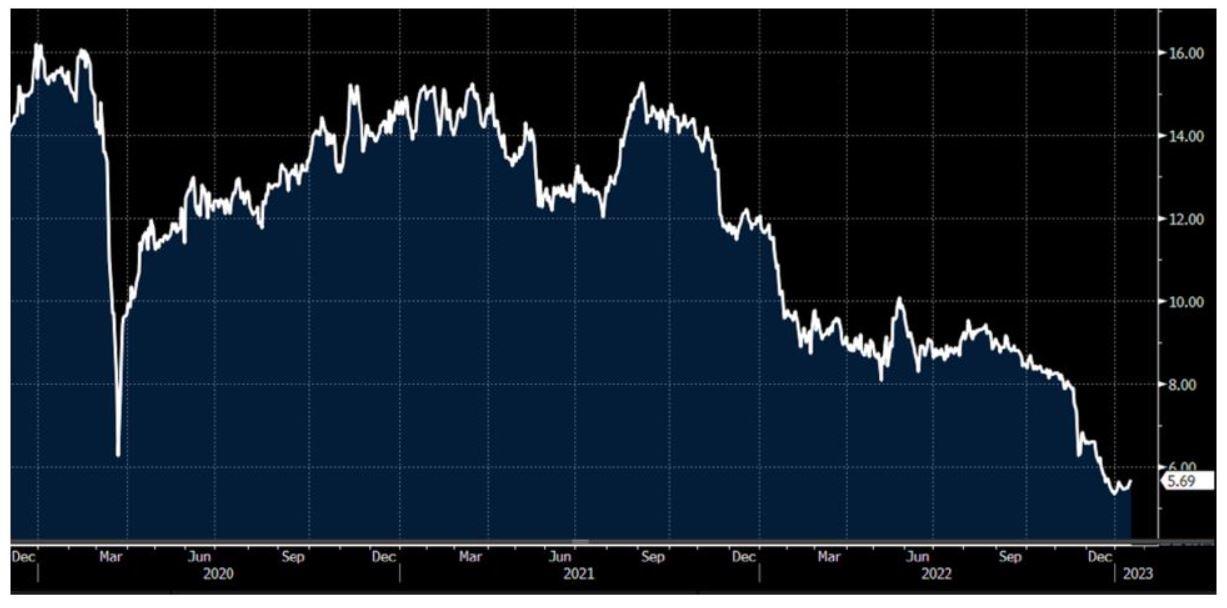

Chart showing Ryman having a tough 2022

Source: Bloomberg

And then we arrive at the final ingredient required to qualify as a potential value trap, the share price must have dropped a lot. In the case of Ryman, the share price is down around 65% lower than its 2019 highs. A large drop in share price is the last and arguably most important requirement of setting a really good value trap. Typically, 50% is a perfect drop but there’s nothing wrong with a +60% drop either. The notion that just because a share is down 50% it must be cheap is a dangerous mindset to have. It can work in your favour; the market does overreact to bad news and investors can be well rewarded for taking advantage of that. But it won’t work every time and those times are generally a value trap.

The problem for investors is that sometimes shares trade at levels wildly over the true underlying value of a business and sometimes the world changes in a way that is detrimental to the value of a business. Either of these happening can easily lead to a 50% drop in share price, with little chance of a quick recovery. One could argue that elements of both apply to Ryman. If New Zealand is beginning a period of several years of flat residential house prices, then it is very unlikely that retirement villages will be increasing the book value of their villages which had been a key driver of historic earnings growth. If this does turn out to be the future for New Zealand property prices then investors that purchased Ryman at $16, based on continued future gains in residential property, will have got it way wrong.

This article is very much an opinion piece about why Ryman could be a value trap, which may or may not turn out to be the case, no one knows for sure. But one certainty is that investors that believe a company must be value solely because its share price is down over 50% are playing a dangerous game because value traps are real.

Share article:

Other Insights

February 2024 - Recent studies show that passive investing now outweighs active investing

Read more >Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Generator Britomart Place

Level 10, 11 Britomart Place

Britomart, Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

2024 Castle Point Funds, Inc. All rights reserved.

Privacy Policy